Banks turn away borrowers to avert bad loans

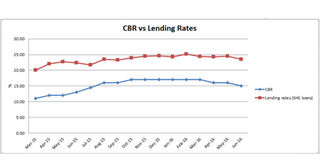

Bank of Uganda (BoU) graphs showing the relationship between the Central Bank Rate and lending rates. BoU Governor Mr Tumusiime Mutebile has, on several occasions, noted that Uganda is a free market economy and BoU cannot regulate rates. (Source of data: Bank of Uganda) GRAPH BY Mark Keith Muhumuza

What you need to know:

Latest indicators show that commercial banks are slowing down on lending to both institutions and individuals because of the increased risk profile of clients due to the headwinds in the economy although Bank of Uganda continues to say all is well.

Kampala. A salaried employee with one of the telecommunication companies walked into a commercial bank to secure a loan at the end of July but to his surprise, he was turned away. He had been a customer of the bank for at least seven years. But the bank denied him a salary loan, asking him to wait for two months for a possible consideration.

In the first half of 2016, indicators are pointing to commercial banks slowing down on lending because of the increased risk profile of clients due to the headwinds in the economy. With the exception of foreign currency loans, the Shilling loans, which most businesses and individuals rely on, have been flat, according to statistics from Bank of Uganda (BoU).

Statistics

According to BoU statistics, total private sector credit stood at Shs11.4 trillion in December 2015 and by June this year, it had marginally increased to Shs11.5trillion. This indicates growth of less than one per cent. Furthermore, figures from two listed commercial banks for the first half of the financial year indicate a similar trend.

In the first half of the year, the loan book for Stanbic Bank Uganda was almost flat, with the bank lending Shs1.87trillion. This is just a one per cent rise from Shs1.85trillion over the same period in 2015. Dfcu Bank loan was one per cent down in the first half of 2016 to Shs759.4b compared to Shs766.8b over the same period in 2015.

The caution commercial banks are taking is a result of the high-interest rate environment that also results into loan defaults.

Factor

“The cause of weak lending to private sector is related to slackness in the economy observed in the same period; the associated increase in non-performing loans (NPLs) which increased from Shs573.4b in December 2015 to Shs803.8b in June 2016; and the tight monetary policy as a result of upsurge in inflation,” Mr Adam Mugume, the executive director research at BoU tells Daily Monitor.

NPLs as a percentage of total loans stood at seven per cent in June 2016, a rate last seen in December 2003. At the end of 2015, several commercial banks such as Crane Bank, Standard Chartered Bank, and dfcu had some of the highest NPLs in the market leading them to make provisions, using their income, to cover for the delayed payment by borrowers. The risk of rising NPLs has led banks to proceed with caution.

“The modifications to our risk appetite where we deliberately slowed down credit growth on most of our retail lending were off the back of the high interest rate environment and our strong credit processes also ensured that we maintained a commendable credit loss ratio of 1.6 per cent, that was lower than the 1.7 per cent recorded as at June 2015. This is well below the industry average,” Mr Sam Mwogeza, the chief finance officer at Stanbic Bank Uganda, said.

Economy in distress?

About a month ago, Daily Monitor published an article on distressed businesses that were seeking help from government. One of the reasons pointed out by the businesses was the high interest rate environment where lending rates are as high as 27 per cent for some commercial banks. There is no bank that is issuing loans at a rate below 20 per cent.

The beginning

All this started in April 2015 when BoU started increasing the Central Bank Rate (CBR), in order to manage the pressure from inflation as a result of the depreciating Shilling. The Monetary Policy Committee (MPC) meeting in April 2015 opted to raise the CBR from 11 per cent in March 2015 to 12 per cent. This first rate hike since November 2011 when the CBR was raised to 23 per cent.

From April 2015 to October 2015, the CBR rose to peak at 17 per cent and remained flat all through to April 2016 when BoU eased it to 16 per cent. The effect of raising the CBR in April 2016 resulted in a hike in the Prime Lending Rate (PLR), from an average of 20.08 per cent to 22.1 per cent. The rise in PLR was at a much a faster pace than the CBR. By November 2015, average PLR had gone up to an average of 24.45 per cent before peaking at 25.22 per cent in February 2016. It should be noted that during the period between November 2015 and February 2016, the CBR remained at a 17 per cent constant but average commercial lending rates kept rising.

BoU has since reviewed its policy downwards, with the last reduction being 100 basis points in August 2016 to 15 per cent. Lending rates from commercial banks are still at an average of 23.54 per cent.

According to Mr Fred Muhumuza, an economics lecturer at Makerere University, reduction in CBR doesn’t exactly translate into an immediate rate reduction.

“A reduction in CBR does not imply an immediate reduction in lending rates as commercial banks may simply decide to ‘wait-and-see’ if the downward trend will continue. However, there are several other rates of interest that affect bank performance as they impact on operational costs and hence profits,” he says.

As rates rise, banks also go slow on lending and start focusing on mobilising deposits from customers. The result is a private sector that is deprived of much-needed investment capital to grow their businesses. For instance, Stanbic Bank Uganda reduced its entire lending to the Personal Business Banking (where most SMEs are financed) segment from Shs1.1 trillion in the first half of 2015 to Shs1.02 trillion in the first half of 2015. This is in part due to the higher risk profile that is placed on such clients.

“The high-interest rate environment is impacting the rate of growth for both corporates and SMEs in the market. This, in turn, hurts growth in the economy,” Mr Herman Kasekende, the chief executive officer (CEO) Standard Chartered Bank, recently explained, adding: “The Private Sector Credit (PSC) is at historical lows due to the interest rate environment. Any further easing in lending rates – on the banking side – and CBR – on the BoU side should bring back confidence in the issuance of PSC. Whenever PSC grows, then it also boosts aggregate demand.”

Banks still profitable

Even when commercial bank lending is not growing as fast as it used to, some banks are not feeling the pinch. Both dfcu Bank and Stanbic Bank have seen record half-year profits. Dfcu’s after tax profit surged 70.7 per cent to Shs23.3b up from Shs13.7b. This was on account of a rise in income on existing loans and the interest income from Treasury bills. The bank was also able to reduce its expenses on provisions for bad debts, which freed up income to generate a profit.

Stanbic Bank Uganda also saw its half-year after tax profit jump 57 per cent to Shs107b from Shs68b. The bank had a mix of contributions towards the growth of the profit and it was driven by increased interest income from the sale of government securities, lending to other banks through the interbank market and then higher yields on loans to customers. However, the bank was also able to increase its income in the non-interest income segment like trading income and fees and commissions.

“We anticipated the impact of these macroeconomic changes and took steps to strengthen the diversity our income lines to compensate for the expected slow-down in Loans and advances interest income,” says Mr Patrick Mweheire, the CEO Stanbic Uganda.

Government rates attractive

Yields on government securities, specifically Treasury bills had attractive rates meaning that the banks opted to lend to the government than the private sector. For instance, Treasury bills bought in January 2016 and matured in June 2016, were generating returns of 20.5 per cent for the 91 days and 23.2 per cent for 182days.

The bankers consider these rates attractive because they are risk-free. The government has committed to borrowing less in 2016/17 and rates for the 91 days and 182 days by July 2016 had dropped to 15.7 per cent and 16.1 per cent respectively.

Market sentiments

The sentiment from the market is that the worst is over for the economy and borrowing will rebound as BoU continues to ease its policy.

“Lending is projected to increase as inflation is projected to decline and stabilise around the five per cent target and therefore monetary policy is now in easing phase, and economic activities are projected to rebound though perhaps at a slow pace because of the complex external environment,” Mr Mugume notes.

Uganda, Kenya leaders’ perspective

In Kenya, President Uhuru Kenyatta signed a law that seeks to cap lending rates within a 4 per cent margin of the CBR. The move, according to President Kenyatta, would go a long way in reducing the cost of credit to the private sector. The Private Member’s Bill is expected to come into force in about 14 days (from Friday last week) and it has generated debated across the region. In Uganda, Prof Emmanuel Tumusiime Mutebile, the BoU Governor, has often been asked to rein in on banks to reduce lending rates to within a margin closer to the CBR. Mr Mutebile has, on several occasions, noted that Uganda is a free market economy and BoU cannot regulate rates. This is the same argument the government is using to insist that lending rates shall not be regulated. Speaking on the sidelines of the 7th CEO Summit at the Kampala Serena Hotel last week, Mr Ruhakana Rugunda, the Uganda Prime Minister, told Daily Monitor there will be no regulation on interest rates.

The numbers

17

The peak percentage CBR rose to in 2015.

14

The current Central Bank Rate announced in August this year.

11.5

Total private sector credit by June this year.

23.54

Average percentage at which commercial banks are currently lending to borrowers.