Prime

Fintechs or banks: Who gets us closer to a cashless future?

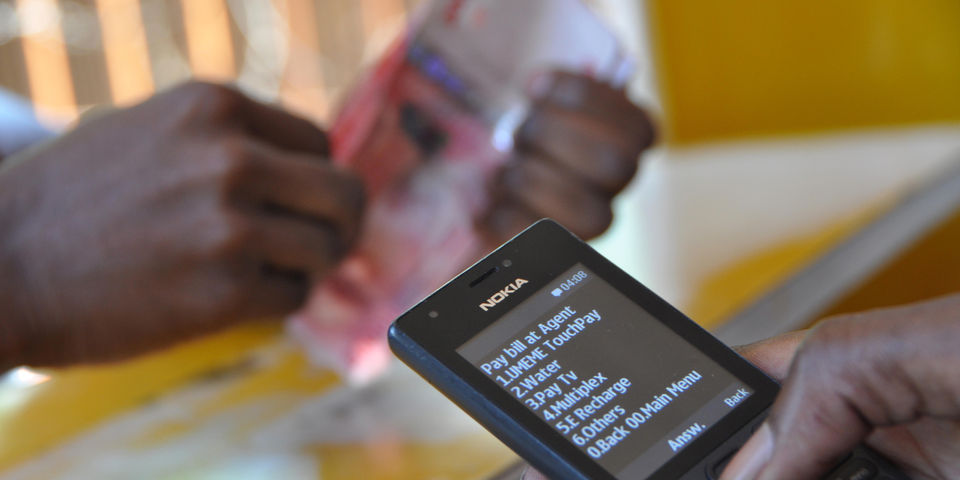

A woman completes a cashless transaction. Financial technologies are disrupting the traditional way that financial firms perform business. Photo / Rachel Mabala

What you need to know:

- As fintechs reshape banking, banks are now in talks with fintechs to consider how they can expand into new channels to retain relevance to their customers and investors. But a large portion of Ugandan traders and consumers are still cash-driven with a few undertaking e-payments.

Kampala has morphed into an East African hub to over 150 financial technology, or Fintech businesses set up in the last decade.

As a result, it is tilting the financial sector for traditional banking and finance executives who dominated the sector for so long.

Today, the country’s big banks are rubbing shoulders, or perhaps competing for business with fintech companies founded less than a year ago.

But, in many cases, it is the fintech entrepreneurs doing the talking, while banking and finance executives do the listening.

For now, the majority of bankers, insurers, and investment managers are responding in a positive way. Most are taking up partnerships with fintech companies.

But it remains to be seen how such partnerships will play out in the future, and whether fintech growth could pose a competitive threat in the finance industry.

Financial technologies are disrupting the traditional way in which financial firms perform business.

A new study on the state of Uganda’s Fintech Industry captures the evolution of financial technology that started almost 25 years ago with the introduction of the Automated Teller Machine in 1997.

The study authored by Financial Technology Service Providers’ Association (FITSPA) shows financial technology has evolved into the mobile money market in 2009, and then into e- commerce in 2014 as Jumia set up in Uganda. Mobile, Agency and internet banking came along the way.

Initially, these technologies were used to optimise the back-end operations of financial services firms, but now they increasingly represent technologies that are transforming traditional financial services, including payments, money transfers, lending and savings, blockchain, advances, and asset management.

Peter Kawumi, the board chair at Fitspa quoting the report says the Covid-19 pandemic came as an opportunity for Uganda as a lot of innovations came through. Such innovations provided a shift to an inward strategy for self-reliance.

Notable among them was the increase in digital payments which were taken up by the people enabling the financial technology community benchmark on that to thrive.

More innovations in the fintech sector are expected in the future with growing digital literacy of the population, coupled with a youthful population pushing for greater adoption of fast, easy financial solutions.

This is evidenced by the ever-growing number of users on mobile money platforms standing at 32 million, according to Uganda Communication figures. The adoption of Fintech services is expected to grow even more in the future.

Additionally, with formal financial inclusion in Uganda standing at just 58 percent, traditional financial service providers clearly face challenges in extending financial services to the unbanked and under-banked population.

Fintech companies have sought to target the gap in access to finance by utilising innovative technology, while simultaneously entering some of the most profitable segments of the financial services value chain.

The business segments that are more profitable, but with lower revenue, include the fees-based business areas such as payment transactions, investment banking, and asset management and insurance.

Their unique offerings, coupled with robust and scalable technologies, have the potential to drive significant gains in financial inclusion.

The rise of smartphone usage has accelerated the use and convenience of managing personal finance at one’s fingertips. More so now, when consumers actively adhere to Covid-19 restrictions.

It is now easier to make money transfers or remittances which remains an integral part of Uganda’s ecosystem, more so, after the Covid-19 pandemic.

The Covid-19 pandemic disrupted livelihoods and fintechs illustrated the need for innovation in the lending market as more people pursue quick unsecured loans, without necessarily going through traditional financial institutions.

It is now easy to access to insurance for property, motor vehicles, medical, and life has seen a sharp uptake in recent years.

Blockchain or crypto Ugandan investors are seeking to invest their disposable income in new opportunities such as the rising cryptocurrency trend.

Micheal Atingi-Ego, the deputy governor at Bank of Uganda believes the technology revolution has transformed service delivery and customer expectations so radically that traditional financial service providers have embraced Fintech for their evolution, with most seeking to leverage electronic platforms and scale down their brick and mortar branch footprint.

“Heeding the reminder by Bill Gates that, “People need banking, not banks”, many financial institutions have been disrupted and have accepted that to survive, they need to be intuitive, innovative, and customer-centric,” Atingi says.

Atingi is of the view that the old ways of delivering finance may not be sustained because consumers find that the processes of traditional players such as banks are too cumbersome to navigate.

Seeing that friction, technology firms have stepped in to meet people’s financing needs conveniently and at scale thereby jolting traditional banks to wake up and join the bandwagon for fear of losing clients’ trust in their ability to act in the public’s interest.

Atingi in a veiled prophesy believes while Fintech is the disrupter today, it will be the established and conventional means to deliver financial services in the future.

This is because of its power to enhance customer experience, strengthen risk management, and improve cost efficiency.

Building trust

As the shift into a cashless digital economy becomes a reality. Atingi says building trust is a shared responsibility among all the actors in the ecosystem.

“FinTechs must be trustworthy so that customers have faith that their money and data are safe with them,” he says.

As it advances, Atingi says in his view that, the industry must manage cyber risk, preferably with common risk management standards for cyber defence; manage information security risk through robust protection of customer data; and avoid the misuse of data analytics and artificial intelligence by ensuring the privacy of data, explainability of results, accountability for decisions, and acceptability of results.

The industry will do very well if it embraces the values of fairness, ethics, accountability, and transparency in the responsible use of data analytics and artificial intelligence in financial services, as it grows in sophistication and scale.

Globally, the study shows the basis of e-commerce is trust. Building on trust, many Ugandan consumers according to the report do not exhibit strong trust in e-commerce, specifically with the online payment through debit or credit card and, or money for products that they have not yet received and verified.

This is magnified by low digital literacy among both the consumers and service providers. Henceforth, fintechs will need to grow consumer trust in their e-commerce platforms through a series of product verification, refund systems, and active customer care helpline.

In addition, a large portion of Ugandan traders and consumers are still cash-driven with a few undertaking e-payments. Working to have digital wallets shall be the next horizon for e-commerce players.

Fintechs can work with traditional banks to bolster this by providing credit or money in e-wallets to the demand and supply side.

Currently, e-commerce is more focused on last-mile delivery leaving other components of the supply chain unserved. Offering business-to-business (B2B) services and support is virgin territory for those wishing to enter what is considered a crowded sector.

Through the development of partnerships with companies such as Mobile Network Operators (MNOs) and banks, Fintechs can tap into a wider customer base and quickly and efficiently increase their reach.

Partnerships with existing incumbents such as banks, microfinance institutions can provide fintechs with new data points that can be used to better understand customers’ needs and risk profiles, ultimately creating tailored products for a targeted customer base.

The Ugandan ecosystem still revolves around mobile technology such as USSD codes and text messages.

This technology simplifies the user interface and increases trust. Fintechs need to capitalise on the flexibility of mobile wallets to scale their growth.

This can be supplemented with cloud technology. It is envisaged that the future of customer service is reliant on the embracement of digital technology to scale operations quickly and efficiently through cloud technology.

This is cost-effective and allows for the replication of business models in other countries.

Opportunities

There are five virgin markets regionally: South Sudan, Burundi, Ethiopia, Somalia, and the Democratic Republic of Congo.

In the research, the Fintech ecosystem illustrated that these countries are ripe for potential Fintechs specifically in payments and remittances. A segment that Fintechs in Uganda are well-versed in and have the experience to undertake in a new country frontier.

DON'T MISS: Why Ugandan startups attract less financing

But more innovation and development needs to be done by existing fintechs to capture the underserved population. The creation of products and services geared towards the people; in this case, the less digitally savvy people would prove fruitful.

The new game plan

Initially, these technologies were used to optimise the back-end operations of financial services firms, but now they increasingly represent technologies that are transforming traditional financial services, including payments, money transfers, lending and savings, blockchain, advances, and asset management.

Trust is the basis

Globally, the study shows the basis of e-commerce is trust. Building on trust, many Ugandan consumers according to the report do not exhibit strong trust in e-commerce, specifically with the online payment through debit or credit card and, or money for products that they have not yet received and verified.